Appraisal clause outcome data finds auto insurers underestimating repair costs by thousands

Data from 46 appraisal clause process outcomes shared with a Texas public adjuster a week ago found insurers’ offers would have left customers short of the total amount needed to fix their vehicles by typically $5,312.46.

Had the consumers not went through appraisal process, the insurers could have incorrectly underpaid claimants by a lot more than $244,000 collectively, in line with the information shared by public adjuster Robert McDorman, gm of Auto Claim Specialists.

The findings McDorman shared with us with some Texas lawmakers can be found here. We redacted the claim numbers and policyholder information to preserve customer privacy, and that we also added fields to investigate the main difference between the original insurer estimate and also the amount decided to following the appraisal process.

“These numbers DO NOT range from the Economic Total Loss claims we handle as Repair or Replace claim type and eventually flip to a repairable vehicle, as it must have experienced the 1st place,” McDorman wrote in an email Monday.

On average, insurers’ settlement offers prior to the appraisal clause invocation were wrong by about 45.86 percent, according to McDorman’s data. The final amounts awarded customers typically were a lot more than double exactly what the insurers had offered.

Under the typical right to appraisal process, either the customer or insurer can has got the right to make use of an appraisal clause within a policy to resolve a dispute within the amount owed inside a claim. Both sides hire an appraiser to judge the automobile separately. If they agree on a dollar value, that amount is binding on everyone. If they can’t come to a resolution, they agree to hire an “umpire” who also conducts an exam from the damage. When the two appraisers agree a treadmill appraiser and also the umpire agree with a sum, that value is binding.

“Within my testimony I stated our average negotiated rise in repair procedure dispute claims we handle is more than 35%, and that we often uncover unsafe repair measures in the insurance carriers’ discounted repair estimates,” McDorman wrote in an email to the Texas House Insurance Committee, which recently evaluated a bill related to appraisal clauses. “By nature, I'm always conservative in my projections. Unlike the entire Loss claims and Inherent Diminished Value claims we handle, where at the stroke of a key we are able to generate a report showing the settlement details of each, the repair procedure dispute claim types require me to manually undergo our database to retrieve the information. These types of claims are extremely technical and require a lot of experience to handle. After our audit of those types of claims from Texas insureds only, we found the typical under-indemnification to become 90%! …

“I needed to supply you and your fellow committee members using the actual under-indemnification on these types of claims and the documents supporting them. ”

Many of the nation’s Top 10 auto carriers are represented in McDorman’s data. The biggest Texas and national auto insurer State Farm isn’t, but that carrier also removed the authority to appraisal for repairable vehicles about four years ago.

“Please be aware State Farm has restricted their insureds from invoking the right of appraisal in contest of loss disputes on repairs regardless of whether the written repair estimate constitutes an unsafe repair,” McDorman wrote towards the committee. “Thus, the 90% settlement increase we see on repair dispute loss types doesn't include State Farm insureds who've disputes within the repair methodology used by State Farm.”

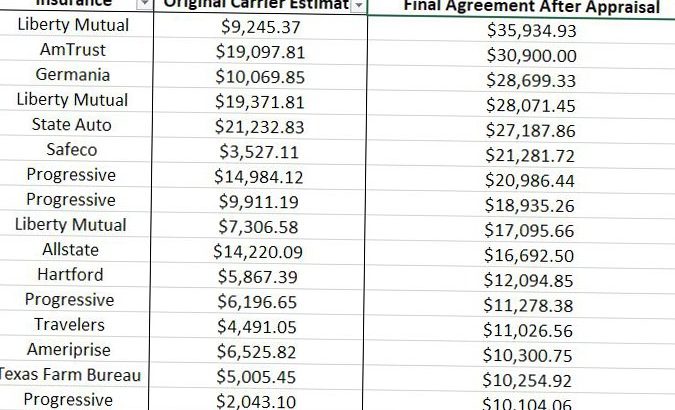

The largest insurer error when it comes to dollar value involved Liberty Mutual underestimating the amount of work required by $26,689.56. The $35,934.93 awarded through the appraisal clause process was nearly four times the $9,245.37 the insurer had asserted it owed for that repair. This appraisal award was the only one in McDorman’s records big enough the consumer wouldn’t have been eligible for Texas small-claims court, that is restricted to disputes of $20,000 or less.

The largest-magnitude mistake was Safeco offering $3,527.11 but ultimately owing their customer $21,281.72 — six times the amount the insurer had originally felt was appropriate.

The smallest dollar-value difference encountered involved Progressive, which held an automobile only needed $1,756.15 in repairs. The appraisal process found $2,447.97 in work was necessary, a difference of less than $700.

The smallest-magnitude disparity saw Liberty Mutual estimating $6,866.53 in repairs and also the work ultimately calculated through the appraisal process at $7,924.93 — an increase of only 15.41 percent.

These lower-dollar claims and McDorman’s data generally would seem to support the appraisal clause bill based on the Insurance Committee and ultimately passed by the Texas House on Friday.

House Bill 2534 would require appraisal clauses in Texas policies for totals and repairable vehicles and force the loser to pay the winner’s fees. This really is in contrast to traditional appraisal clauses requiring both sides to cover their respective appraiser expense and split the umpire bill.

Under HB 2534, when the insurer’s estimate is $1 or more short, they must cover the customer’s reasonable appraisal costs. Both sides would still split the cost of the umpire if a person was needed.

This “loser pays” provision might make exercising the right to appraisal more feasible and practical for consumers on smaller-dollar disputes. Under the traditional “each side pay” setup, using small-claims court to address such arguments might make more financial sense.

McDorman, for example, said his firm charges about $800 for a total loss appraisal.

In another email towards the Insurance Committee, McDorman agreed that “a very small percent” of claims visit appraisal, but he argued that this reflected a lack of consumer knowledge. “I have spoke with a large number of insureds through the years, and I haven't yet listen to a single one who had been relayed through their carrier about their right to invoke appraisal,” he wrote. “The percent of insureds who request appraisal is currently small because hardly anyone knows about this right. This really is something that hopefully publicity from this bill will help change.”

A Winnsboro, Tex., repairer told lawmakers the appraisal process is frequently necessary to make her customers whole on auto repair claims.

“Our clients are having to invoke their appraisal clause at least 50% of times to obtain proper repairs,” Griffin’s Paint & Body owner Crystal Griffin wrote meant for HB 2534. “Whether it were not for your option our customers could be left to foot the balance by 1000s of dollars and/or we would go into our pockets much more than we already do to help our community. The general public is under the impression that once they pay their deductible, the insurers will take care of the rest that is active in the proper repair of the vehicle. Because it is now, that’s just not the situation and also the appraisal clause is the only option they have to make them whole per anything they entered into with their insurance provider.”

Even if the data here doesn’t reflect the average repairable vehicle claim, the fact that insurers can make these types of errors continues to be an enormous concern for body shops and consumers. It’s additionally a reason for favor of empowering consumers with HB 2534.

These findings also ought to worry insurance actuaries, regulators, reinsurers and claims executives too. If in-house adjusters or subcontracted estimators could be this inaccurate even some of the time, just how much are reserves and potential loss risk being underestimated?